Profit sharing is part of variable pay that enables employees to particitpate on company’s success. As the name states it makes sense only for companies in profit.

Example #1:

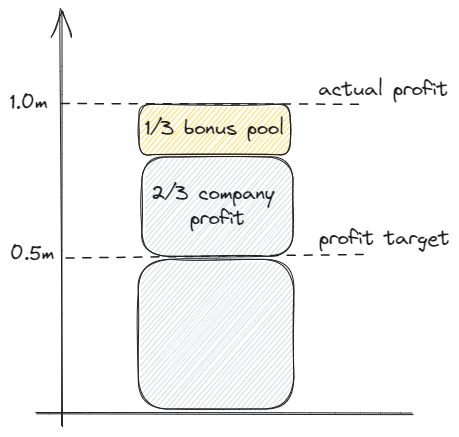

Company sets a profit target of $0.5 mil. It allocates 1/3 of ‘anything above the profit target’ to a bonus pool. The bonus pool is distributed to employees to cover their bonus. The bonus is always distributed pro-rata based on everybody’s (fixed) salary.

There are 3 attributes to profit sharing:

i) profit target: you need to set realistic goals

ii) profit sharing: how much profit do you want to keep & share?

iii) size of employee bonus: how much additional money can employees make if company is in profit?

Example #2:

Company sets a profit target of $0.5 mil. It allocates 1/3 of ‘anything above the profit target’ to a bonus pool. Employees can earn 1 extra monthly salary from the Profit sharing. If bonus pool does not cover full monthly salaries, employees get pro-rata share of available money.

You can distribute profit sharing also on quarterly basis. Just set quarterly profit targets and recalculate profit sharing and bonus pool to quarterly salaries. In a sum, profit sharing bonus should amount up to 15% of annual pay.

Example #3:

Company sets quarterly profit target of $0.125 mil. It allocates 1/3 of ‘anything above the profit target’ to a bonus pool. Each quarter employees can earn up to 25% extra monthly salary from the Profit sharing. If everything goes well, employees make 4x 25% monthly salary = 1 extra monthly salary in year. Each quarter actual profits are compared to profit targets. 1/3 of anything above is allocated to quarterly bonus pool and distributed to cover 25% of monthly salaries. Not more. If not enough money is available, bonus pool is distributed on pro-rata basis.

Critical considerations:

- profit sharing can be based on free cash flow, EBITDA, operating profit, or any non-gaap metric

- recommended frequency: 6 months or quarterly

- quarterly results are cumulative, i.e. loss in Q1 is forwarded to results in Q2. Also, bonus for Q1 is recognized as expense in Q2 results.

- if bonus pool is greater than (capped) bonuses, undrawn bonus pool is not brough forward to next period