Equity compensation is the most meaningful form of performance compensation. Early stage tech companies also use company equity to retain and attract talent (that they would not be able to pay fully in cash). Publicly traded companies use performance stocks to align and incentivise employees (mostly executive team) to create shareholder value.

Publicly traded companies

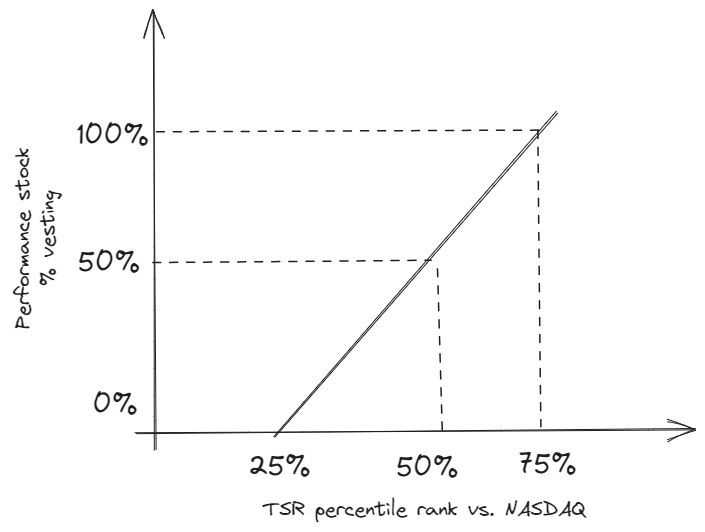

The equity compensation plays significant role in senior executive team. Subject to market capitalization, the individual equity component can be anywhere from 10x to a few hundred times the fixed salary. It is usually comes in form of a performance stock ad the most common performance trigger is total shareholder return (TSR). TSR is stock value appreciation over specific period of time. The results is then compared to the performance of the stock market (S&P500 or NASDAQ).

Startups

Total amount of equity compensation depends on company’s latest valuation. Higher the valuation, more generous you can be with equity compensation. In early stages, companies typically allocate 10-15% of the company’s equity (which can increase to 20% after Series A) to employees. In seed stage, key roles receive 80-100% of their annual salary in equity. As a result, total equity awards range from 1% for senior key roles to 0.01% for junior non-critical roles. With increasing company valuation, the equity component rises in value and can be come 10x the annual salary.

You should use back-loaded vesting schedule: 10:20:30:40% per year with 1 year cliff. To preserve your equity pool, leaving employees have 90 days to excercise the option or loose their grants. There are many more details to equity compensation. I recommend to read the guide by Index Ventures.

There are many forms of equity compensation with different tax implications:

Restricted stock units (RSU)

An RSU is a promise from your employer to give you shares of the company’s stock (or the cash equivalent) on a future date—as soon as you meet certain conditions. Example: Company

An example of restricted stock/units: Your company grants you 2,000 RSUs when the market price of its stock is $18. By the time the grant vests, the stock price has risen to $20. The grant is then worth $40,000 ($20 x 2000) before taxes. You can sell/hold onto them once they’ve vested.

Taxes on restricted stock/units: With RSUs, you’ll be charged income tax at vesting and CGT (if any) at sale. With RSAs, you’ll be taxed at the time of grant and sale under section 83b election rules.

Performance shares/units

Performance shares/units are less frequently granted to other employees but are significant for executives (see the chart above). It’s because they’re effective to align you with company performance, incentivizing you to focus on achieving strategic objectives and creating shareholder value.

An example of performance shares/ units:

Your company grants you 2,000 performance shares that will result in 2,000 shares if the EPS of your company grows by 10% per year.

Taxes on performance shares/ units:Performance stock units (PSUs) have similar tax events to RSUs while performance stock awards (PSAs) have similar tax events to RSAs.

Stock Options

Stock options provide you with the right to purchase a certain number of shares at an initially agreed price (i.e. exercise price) at a future date after vesting. ISOs and NSOs are the two common forms of employee stock options. ISOs are more tax favorable than NSOs but are more restrictive such as grant and eligibility limitations.

An example of stock options:

Your company grants you 2,000 shares of stock options. If your exercise price is $20 per share and the current share price is $40, then your shares are worth $20 per share ($40 – $20). The total value of your stock options is now $40,000 ($20 x 2,000). Once they’ve vested, you can exercise (i.e. purchase) your share and sell/hold onto them.

Taxes on stock options:

For NSOs (with a fair market value that cannot be readily determined), the tax implications are simpler – ordinary income tax at exercise and CGT at sale.

For ISOs, no income is recognized for the regular tax at exercise but you may have to pay an Alternative Minimum Tax (AMT). If you satisfy the holding period requirement, you only have to pay long-term CGT at sale. Otherwise, you’ll pay ordinary tax and short-term capital